US Online Casino Legal States 2026: Your Step-by-Step Launch Playbook

Which US states have legal online casinos in 2026?

Seven states have active real-money online casino frameworks in 2026: New Jersey, Pennsylvania, Michigan, Connecticut, West Virginia, Delaware, and Rhode Island (live since March 2024, still ramping). Several others — New York, Illinois, Indiana, Maryland, and California — have bills in motion but no enacted legislation yet. If you're planning a US market entry, these seven are your only legal options right now.

New Jersey has been live since 2013 and remains the most mature market by operator count and supplier depth. Pennsylvania went live in 2019 and overtook New Jersey in gross gaming revenue by 2022 — it's now the largest regulated iGaming state by GGR, though its tax structure is brutal (more on that below). Michigan launched in January 2021 and has grown steadily, particularly strong on slots and live dealer. Connecticut followed in October 2021 under a compact with the Mashantucket Pequot and Mohegan tribes. West Virginia has been live since 2020 but remains a small market; the five licensed casinos tether their skins to DraftKings, BetMGM, and a handful of others. Delaware was technically first (2013) but the market is tiny — three casinos, state-run lottery model, minimal commercial opportunity.

Rhode Island is the newest entrant worth watching. The state authorized iGaming in 2023 and Bally's went live in March 2024 under an exclusive contract with the Rhode Island Lottery. That exclusivity model means there's no open operator market there — file it under 'monitor, don't enter.' The real near-term expansion plays are New York and Illinois. New York's iGaming bill has passed committee multiple times; the state's sports betting revenue gives Albany a clear reference point for what regulated online casino could generate. Illinois is further behind legislatively but has a massive land-based footprint that would support tethering. Neither has enacted legislation as of mid-2025, so don't build your 2026 business plan around either.

If you're a first-time operator doing market selection, my honest recommendation is New Jersey or Michigan. New Jersey's DGE process is well-documented, the supplier ecosystem (platform, games, payments, KYC) is the deepest in the US, and the player acquisition market is competitive but understood. Michigan is slightly less crowded and the Michigan Gaming Control Board (MGCB) has been pragmatic in its licensing approach. Pennsylvania's GGR is tempting but the 54% effective tax rate on slots means your unit economics look very different than they do offshore.

| State | Live Since | Regulator | Slots Tax Rate | Table Games Tax Rate | Land-Based Tethering Required |

|---|---|---|---|---|---|

| New Jersey | 2013 | DGE (Division of Gaming Enforcement) | 15% | 15% | Yes — Atlantic City casino |

| Pennsylvania | 2019 | PGCB (PA Gaming Control Board) | 54% | 16% | Yes — PA licensed casino |

| Michigan | 2021 | MGCB (MI Gaming Control Board) | ~20–28% | ~20–28% | Yes — commercial or tribal |

| Connecticut | 2021 | CTHC / Tribal compacts | 18% | 18% | Yes — Mohegan or Mashantucket only |

| West Virginia | 2020 | WVLCB (WV Lottery Commission) | 15% | 15% | Yes — one of 5 licensed casinos |

| Delaware | 2013 | Delaware Lottery | ~43.5% | ~43.5% | Yes — state lottery model |

| Rhode Island | 2024 | Rhode Island Lottery | 51% | 51% | Yes — Bally's exclusive contract |

What is the land-based tethering requirement and how does it affect your launch?

Every US state that has legalized online casino requires operators to partner with — or be owned by — an existing land-based casino licensee. You cannot obtain a standalone iGaming license. This tethering requirement is the single most important structural constraint for any new market entrant: it means your first call is to a casino partner, not a platform vendor.

The tethering model exists because US states legalized iGaming as an extension of their existing land-based regulatory frameworks, not as a new vertical. The land-based licensee holds the 'master' license and is ultimately responsible to the regulator. Online operators either operate as a 'skin' under that master license (revenue share model) or acquire a land-based property themselves (capital-intensive, but gives full control). In New Jersey, for example, the law requires every internet gaming permit to be held by or affiliated with an Atlantic City casino licensee. DraftKings operates under the Golden Nugget AC's license; BetMGM under Borgata's.

For a first-time operator without a land-based footprint, there are two practical paths. The first is a commercial agreement with an existing licensee — you pay them a revenue share (typically 2–5% of GGR, sometimes structured as a flat fee) in exchange for operating under their permit. This is how most new skins enter the market. The second path is acquiring or investing in a land-based property, which is how some larger operators have structured long-term US plays — but that's a $50M+ conversation, not a startup move.

The practical implication: before you engage a platform vendor, before you start the license application, you need a signed letter of intent from a tethered casino partner. Regulators won't process your application without it. This is the step that surprises most first-time operators coming from offshore markets where a B2C license is a direct relationship between operator and regulator. In the US, that intermediary land-based partner is non-negotiable, and finding one willing to take on a new, unproven operator takes time — budget 3–6 months just for that conversation.

How do you actually get a New Jersey online casino license?

New Jersey's DGE issues Internet Gaming Permits, not standalone licenses. The process runs through the Casino Control Commission (CCC) and requires a transactional waiver or full casino service industry enterprise (CSIE) license depending on your role. Realistically, plan for 12–18 months from application submission to go-live, and a legal and compliance budget of $500K–$1.5M before you flip a single card.

The New Jersey process has two tracks. If you're operating as a 'permit holder' — meaning you're the brand running the casino skin — you need an Internet Gaming Permit issued under N.J.A.C. 13:69O. This requires a qualifying casino licensee partner (your tethered Atlantic City property), a detailed business plan, financial disclosures for all principals with 10%+ ownership, a technical system submission reviewed by the DGE's technical standards group, and an AML/responsible gambling compliance framework. The DGE's technical review alone can take 6–9 months for a new platform — they test every game, every payment flow, every player protection mechanism.

The CSIE license track applies to platform providers, game suppliers, and payment processors who want to operate in New Jersey. If you're using a platform like SoftSwiss, Kambi, or EveryMatrix, they need their own CSIE certification before their software can go live under your permit. Most major B2B suppliers are already certified or in process, which is another reason NJ's supplier ecosystem is the deepest — the barrier to entry for suppliers has been cleared over 10+ years. For a new operator, this means you should prioritize platform and game suppliers who are already NJ-certified; adding a non-certified vendor adds 6–12 months to your timeline.

Costs: the permit application fee is relatively modest (around $400 for the initial filing), but that's not where the money goes. Legal fees for a full NJ application with a boutique gaming law firm run $200K–$600K. The required surety bond is typically $500K. Technical compliance testing and certification adds another $100K–$300K depending on your stack complexity. Then there's the ongoing annual permit fee and the cost of maintaining a registered agent and compliance officer in-state. Budget $1M–$2M in pre-revenue compliance spend for New Jersey, and that's before platform, marketing, or working capital.

How does Pennsylvania's 54% slots tax actually affect your business model?

Pennsylvania taxes online slots at 54% of GGR — the highest effective rate of any regulated online casino market in the world. Table games sit at 16%. This isn't a typo and it's not negotiable. Your entire revenue model for PA needs to be stress-tested against that rate before you commit to the market.

The Pennsylvania iGaming tax structure was set by the Pennsylvania Race Horse Development and Gaming Act amendments in 2017. The 54% rate on slots GGR was a political compromise designed to protect land-based slot revenue — legislators wanted to ensure online didn't cannibalize physical casinos. The unintended consequence is that online operators in PA run on razor-thin margins for slots, which typically make up 70–80% of an online casino's GGR. At 54% tax plus the platform fee (typically 15–25% of GGR on white-label), plus payment processing (2–4%), plus marketing, your effective take-home on slots GGR can be under 10% before overhead.

The math works if you have scale. DraftKings, BetMGM, and FanDuel can absorb the PA tax because their cross-sell economics (sports betting to casino, or vice versa) and brand recognition drive low CAC at high volume. A new operator without an existing player base faces a brutal CAC environment in PA — the established brands have years of first-mover advantage and loyalty programs deeply embedded with the player pool. I've seen operators model PA on offshore GGR margins and then get a very unpleasant surprise when the first tax bill arrives.

My honest take: Pennsylvania is a market for operators who already have a significant US player base to migrate, or who have a clear cross-sell product (like a major sportsbook). For a first-time US operator, start in New Jersey or Michigan where the tax structure is survivable at smaller scale, build your operational competency, and then use that track record to negotiate a PA land-based tethering deal from a position of strength. The PGCB application process is also slower than NJ's DGE — budget 18–24 months for PA from application to go-live.

What does Michigan iGaming look like as a market entry option?

Michigan is the most operator-friendly of the major US iGaming states for new entrants. The MGCB has processed licenses efficiently, the tax rate is tiered and manageable (roughly 20–28% effective on slots), and the market has genuine scale — Michigan's iGaming GGR has consistently ranked second or third nationally. It's my top recommendation for first-time US operators with a realistic budget.

Michigan's Lawful Internet Gaming Act, signed in December 2019 and live from January 2021, allows both commercial casinos (Detroit's three — MGM Grand Detroit, MotorCity Casino, and Greektown) and tribal casinos to tether online skins. The tribal angle is significant: Michigan has more federally recognized tribes with gaming compacts than almost any other state, which means more potential tethering partners and potentially more flexibility in deal terms. Operators like BetMGM, DraftKings, FanDuel, and several smaller brands have all launched under tribal tethering arrangements.

The MGCB's licensing process is thorough but predictable. The Supplier License (for platform and game providers) and the Internet Gaming Operator License (for the brand) run in parallel, and the MGCB has published detailed technical standards that give applicants a clear compliance checklist. From a complete application submission, operators typically see 9–15 months to approval — faster than Pennsylvania, comparable to New Jersey. The MGCB has also been willing to engage in pre-application meetings, which is genuinely useful for first-timers who want to pressure-test their compliance posture before committing to the full application.

One nuance worth flagging: Michigan's tax structure is tiered by GGR bracket, running from 20% at the low end to 28% at higher revenue levels, plus an additional 8% that goes to the tribal casino or commercial partner. The effective combined rate is more complex than the headline number suggests — get your gaming accountant to model the full waterfall before finalizing your pro forma. The player market itself skews heavily toward slots (as everywhere in the US), and Michigan's player acquisition environment is competitive but not as saturated as New Jersey. There's still room for a well-positioned new brand, particularly one with a differentiated game mix or a strong live dealer offering.

What are the realistic timelines and costs for a US iGaming market entry?

A full licensed entry into any US iGaming state — your own operator license, your own platform, your own brand — takes 18–30 months and costs $3M–$8M before you reach break-even. A white-label skin under an existing licensee compresses that to 6–12 months and $500K–$2M upfront, but you're capped on revenue share and brand control. Neither path is cheap or fast.

Let me break down the full-license path in concrete phases. Phase one is market selection and partner identification: 1–3 months to select your target state, negotiate a tethering agreement with a land-based partner, and retain a gaming law firm with active practice in that state. Phase two is application preparation: 3–6 months to compile the application package — financial disclosures, business plan, AML/RG policies, principal background investigations (which the FBI and state police run, not you). Phase three is regulator review: 6–12 months for the regulator to process and approve, longer if they issue deficiency notices. Phase four is technical certification: 3–6 months for platform and game certification, running in parallel with phase three where possible. Phase five is soft launch and ramp: 2–3 months of limited operation before full marketing spend. Total: 15–30 months depending on state and how clean your application is.

The white-label skin path is fundamentally different. Here you're operating under an existing licensee's permit as a 'sub-licensee' or 'skin.' The licensee has already done the heavy regulatory lifting. Your job is to pass a suitability review (lighter than a full license investigation), integrate with the licensee's chosen platform, and launch. Platforms like SoftSwiss's Jackpot Factory model, or the white-label programs run by Rush Street Interactive or Golden Nugget Online Gaming, can get a new skin live in 6–9 months. The trade-off: you typically give up 30–50% of GGR to the platform/licensee combined, you have limited control over the game mix and payment methods, and you're building brand equity on someone else's infrastructure. If the licensee exits the market or changes terms, you have limited leverage.

A realistic cost breakdown for a New Jersey full-license entry: legal and compliance ($500K–$1.5M), technical certification ($150K–$400K), platform setup and integration ($300K–$800K depending on whether you're licensing a turnkey platform or building custom), initial marketing and player acquisition ($500K–$2M for the first 12 months), working capital and operational overhead ($500K–$1M). Total: $2M–$5.7M before you hit sustainable GGR. These are ranges, not guarantees — operators who've tried to do this on the cheap have consistently found that the regulatory and technical requirements don't flex.

| Factor | Full Operator License | White-Label Skin |

|---|---|---|

| Timeline to live | 18–30 months | 6–12 months |

| Upfront cost estimate | $3M–$8M+ | $500K–$2M |

| Revenue share retained | ~70–80% of GGR (after tax) | ~40–60% of GGR (after tax + platform/licensee fees) |

| Brand control | Full — your brand, your product | Limited — platform and licensee constraints apply |

| Game/payment flexibility | High (subject to certification) | Low to medium — depends on licensee's approved stack |

| Regulatory risk ownership | You hold the license — full exposure | Shared — licensee is primary permit holder |

| Exit / portability | License is yours to maintain or sell | You own the brand, not the license — harder to exit cleanly |

| Best for | Operators with US-scale ambitions and capital | First movers testing the market with limited capital |

Which platform and technology providers are actually certified for US iGaming?

The US-certified platform and supplier ecosystem is smaller than offshore but growing fast. SoftSwiss, Scientific Games (now Light & Wonder), IGT, Everi, and GAN are the established names. For game content, the major certified studios include Evolution (live dealer), NetEnt, IGT, Scientific Games, and Aristocrat. Verify certification status with the specific state regulator — it changes quarterly.

The certification requirement is the biggest technology constraint for US operators. Every piece of software that touches real-money gameplay — the platform RGS, the games themselves, the RNG, the payment processing layer — must be independently tested and certified by a state-approved testing laboratory (GLI, BMM, Gaming Laboratories International are the main ones) and then approved by the state regulator. This is not a one-time process; each state has its own certification, so a platform certified in New Jersey needs separate certification in Michigan and Pennsylvania.

For platform technology, the operators who've moved fastest in the US have typically used one of three approaches: licensing a platform from a US-experienced provider like GAN (which powers several US skins), building on Scientific Games' OpenGaming platform, or using the white-label infrastructure of an existing US licensee like Rush Street Interactive (which operates BetRivers and has white-labeled to partners). EveryMatrix and SoftSwiss, dominant in European and offshore markets, have been pursuing US certifications but operators should verify current state-by-state status directly — don't rely on a vendor's sales deck for certification claims.

Game content is where the US market diverges most sharply from global norms. Many popular offshore game studios — Pragmatic Play, Play'n GO, Hacksaw Gaming — have been pursuing US certification but availability varies by state and is still incomplete as of 2025. The safest content strategy for a US launch is to anchor your game lobby on fully certified studios (IGT, Scientific Games, Aristocrat, Evolution for live dealer) and add certified third-party content as it becomes available. Don't assume a studio's global certification means anything in a specific US state — it doesn't.

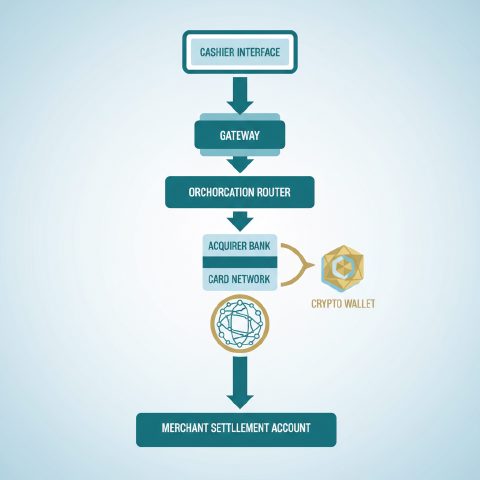

How do payments and banking work for licensed US online casinos?

US online casino payments are more complex than offshore, but far more stable. ACH (bank transfer), Play+ prepaid card, PayPal, and Visa/Mastercard debit are the dominant methods in live states. Credit card deposits are effectively dead in the US — most processors decline them. The good news: with a proper state license, you're not fighting the UIGEA gray zone that kills offshore operators' banking.

The Unlawful Internet Gambling Enforcement Act (UIGEA) of 2006 is the federal law that makes offshore gambling payments a nightmare — banks are required to block transactions to unlicensed gambling sites. A state-licensed operator is explicitly carved out from UIGEA's restrictions, which means you can maintain real bank accounts, work with mainstream payment processors, and offer players stable, familiar deposit methods. This is one of the most underappreciated advantages of operating in a licensed US state versus offshore.

In practice, the payment stack for a US licensed casino looks like this: ACH/bank transfer is the workhorse — low cost, high limits, but 1–3 day settlement. Play+ (a Sightline Payments product) is the dominant prepaid card solution in the US iGaming market, used by DraftKings, FanDuel, BetMGM, and most major operators; it enables instant deposits and same-day withdrawals and is worth integrating from day one. PayPal has been available in New Jersey since 2019 and has expanded to other states — it's a meaningful trust signal for new players. Visa and Mastercard debit work, but approval rates vary by issuing bank and you'll see 10–20% declines on first attempts. VIP Preferred (ACH via Everi) is worth adding for high-value players.

Cashiering speed is a competitive differentiator in the US market. Players expect same-day or next-day withdrawals; the operators who lag on this lose retention. Budget for a proper cashiering integration — don't bolt on a payment layer as an afterthought. Also factor in KYC/AML requirements: every US state requires identity verification at registration (not just at withdrawal), which means your KYC provider (Jumio, Socure, Onfido are common choices) needs to be integrated into the registration flow. Friction here costs you conversion, so test it hard before launch.

What's the outlook for new US iGaming states launching by 2027?

New York is the most likely next state to legalize online casino, with Illinois and Indiana close behind. None are certain — US iGaming legislation has a long history of stalling in committee. Operators should monitor but not build launch plans around unlegislated states. The smarter move is to establish in an existing state now and be positioned to expand when new markets open.

New York is the biggest prize. The state generated over $2B in sports betting GGR in its first two full years, giving legislators a concrete proof point for what regulated online casino could add to state coffers. The iGaming bill in New York (backed by Governor Hochul's administration in various forms) has proposed a 35% tax rate — lower than Pennsylvania, higher than New Jersey. The land-based tethering requirement would likely apply, with New York's commercial casinos (including the three downstate licenses being awarded) as the anchor partners. If New York passes legislation in 2025 or 2026, expect a 12–18 month runway before the first operators go live.

Illinois has a massive land-based footprint (Rivers Casino, Hard Rock, and the Chicago casino project) and a state government that has shown willingness to expand gaming. The legislative path is less clear than New York's — there's no single champion bill moving through Springfield as of mid-2025 — but the commercial logic is undeniable. Indiana, Maryland, and Georgia are further behind but have seen repeated bill introductions. California remains the wildcard: the tribal gaming lobby is the most powerful in the country there, and any iGaming legislation would need tribal buy-in, which makes the politics uniquely complex.

My operational advice: if you're building a US iGaming business, don't wait for New York. Launch in New Jersey or Michigan now, build your operational infrastructure, accumulate the regulatory track record that will make you a credible applicant when new states open, and have your expansion application ready to file on day one of a new state's licensing window. The operators who move first in a new state — as DraftKings and FanDuel demonstrated in sports betting — capture a disproportionate share of the player base that's hard to dislodge. Being second or third into a new state is a very different business than being first.

What are the responsible gambling and compliance requirements operators consistently underestimate?

Every US iGaming state mandates responsible gambling tools — deposit limits, session limits, self-exclusion integration with the state's RG registry — and they're not optional features you add post-launch. AML programs, SAR filing procedures, and geolocation compliance (blocking players outside state borders) are equally non-negotiable. Operators who treat these as checkbox items rather than operational infrastructure get fined or lose their permits.

Geolocation is the compliance requirement that surprises offshore operators most. Because US iGaming licenses are state-specific, you must verify that every player is physically located within the state's borders at the time of each session — not just at registration. This requires a real-time geolocation service integrated into your platform. GeoComply is the dominant provider and is required by most state regulators; it's not a negotiable vendor choice. GeoComply's SDK needs to be embedded in your web and mobile clients, and your platform must handle geolocation failures gracefully (blocking the session, not crashing the app). Budget $0.10–$0.30 per monthly active user for geolocation costs — it adds up at scale.

Self-exclusion integration is equally mandatory. New Jersey operates the statewide self-exclusion registry through the DGE; Michigan has its own through the MGCB. When a player self-excludes, your system must block them within the timeframe specified by regulation (typically 24–72 hours of the exclusion being registered). Failure to block a self-excluded player is one of the most common causes of regulatory fines in US iGaming — it's also a reputational catastrophe. This isn't a feature you can build in the last sprint before launch; it needs to be architected into your player account management system from day one.

AML compliance in the US is governed by the Bank Secrecy Act (BSA), and online casinos are 'financial institutions' under FinCEN's rules. You need a written AML program, a designated compliance officer, SAR (Suspicious Activity Report) filing procedures, and annual independent AML audits. The threshold for SAR filing is $5,000 in suspicious transactions — lower than many operators expect. Most platform providers offer AML monitoring modules, but the compliance program itself is your responsibility, not the vendor's. Hire a dedicated compliance officer before you go live, not after your first regulatory inquiry.

Comments

No comments yet — be the first.