iGaming Payments: How to Build an Online Casino Payment Gateway Stack That Actually Converts in 2026

Building a payment stack for an online casino is harder than picking a processor — it's a multi-layer architecture decision that determines your conversion rate, chargeback exposure, and regulatory standing from day one. This guide breaks down exactly how to structure it.

An online casino payment gateway is the technical and commercial layer that authorises, routes, and settles player deposits and withdrawals. Unlike standard e-commerce, casino transactions carry MCC 7995 — a high-risk merchant category code that triggers automatic refusals at most mainstream processors, mandatory AML screening, and rolling reserve requirements that can lock up six figures in working capital.

At launch, you need Visa/Mastercard card processing, at least one dominant local alternative payment method for your target market, and a crypto rail covering Bitcoin and USDT at minimum. Everything else — e-wallets, bank transfer, vouchers — depends on your jurisdiction. Trying to support 30 methods on day one is a distraction; nail the top three for your market first.

iGaming acquiring works through a small pool of high-risk specialist processors willing to underwrite MCC 7995 merchants. They charge elevated MDRs (3–6%), hold rolling reserves (5–10% of monthly volume for 90–180 days), and require your license, AML policy, and sometimes a personal guarantee before approval. Most operators get declined by three processors before finding one that will board them.

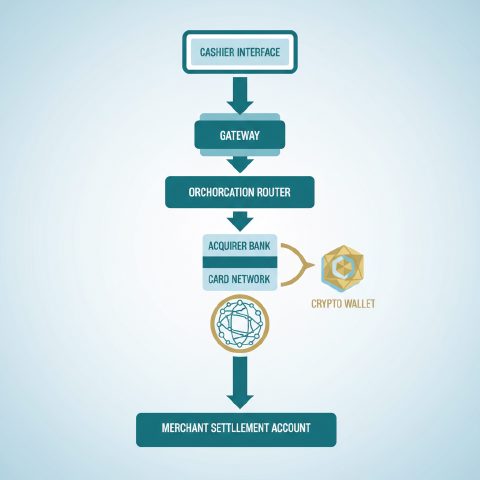

Payment orchestration is a routing layer that sits between your cashier and your acquirers, dynamically directing each transaction to the processor most likely to approve it based on card BIN, country, amount, and real-time decline data. For any casino processing more than €200,000/month in card volume, orchestration typically recovers 15–30 percentage points of declined transactions — that's direct revenue, not a marginal improvement.

Your license jurisdiction is the single biggest determinant of which acquirers will board you, what AML/KYC checks you must run at the payment layer, and whether mainstream e-wallets like PayPal or Skrill will work with you. A Curaçao-licensed operator and an MGA-licensed operator are almost building different payment stacks — the acquirer pool, the reserve requirements, and the compliance obligations differ substantially.

Accept crypto through a dedicated iGaming crypto payment processor — not a generic exchange API — so that transaction monitoring, wallet screening, and KYC linkage are built into the flow. The compliance nightmare operators create for themselves is accepting crypto without screening wallets against sanctions lists and high-risk addresses, which is both an AML failure and a chargeback-equivalent risk when regulators audit.

Expect €15,000–50,000 in setup costs (integration, compliance tooling, reserve capital) and ongoing operational costs of 4–8% of gross payment volume, plus fixed monthly fees for orchestration, fraud tools, and AML monitoring. The rolling reserve is the hidden working capital cost that most first-time operators underestimate — model it as a six-month cash lockup of 5–10% of projected card volume.

Payout speed is a direct retention driver: operators with same-day or instant withdrawals consistently show higher lifetime value and lower churn than those with 24–72 hour manual review queues. The architecture question is whether you process withdrawals through the same rails as deposits or build a separate payout stack — for card operators, you often need both because card refunds are slow and many players prefer a different withdrawal method.

The five mistakes I see most often: launching with a single acquirer and no failover, not enabling 3DS2 (which tanks approval rates on EU cards post-PSD2), building a cashier that requires too many steps before a player can deposit, ignoring local payment methods in favour of cards that have 35% approval rates in the target market, and not monitoring chargeback rates weekly until they're already in Visa's monitoring program.

Evaluate payment providers on five criteria in this order: regulatory compatibility with your license, acquirer network and approval rate data for your target market, integration quality (API documentation, sandbox environment, support SLA), fee structure including hidden fees like FX spread and dispute fees, and financial stability. The onboarding process typically takes 4–12 weeks — plan for it in your launch timeline, not as an afterthought.

Explore the launch guides

listicle

listicle

Best iGaming Payment Providers 2026

Choosing the wrong casino payment provider in 2026 can quietly kill your conversion rate before you even notice. This guide ranks the top iGaming payment solutions by what actually matters to operators: approval rates, integration depth, licensing fit, and total cost.

pillar

pillar

Online Casino Payment Gateway Guide 2026

Choosing the wrong online casino payment gateway doesn't just hurt conversion — it can freeze your funds, kill your license, or lock you into a contract you can't exit. This guide cuts through the sales decks.

spoke

spoke

Online Gambling Merchant Account Complete Guide

Getting an online gambling merchant account approved is harder than most vendors admit. This guide covers the real requirements, costs, reserve structures, and provider options operators face in 2026.

spoke

spoke

iGaming Payment Solutions for Operators

Choosing the right iGaming payment solution is the single most consequential back-office decision you'll make after licensing. This guide cuts through the vendor pitch decks and gives you the real architecture, costs, and trade-offs behind a payment stack that actually converts.

spoke

spoke

iGaming Payment Processing How It Works 2026

iGaming payment processing is the single most fragile part of any casino launch — the wrong stack kills conversion before a player ever deposits. This guide breaks down every layer, from acquiring to crypto rails, with real provider names and operator trade-offs.

spoke

spoke

iGaming Payment Processing

Getting your iGaming payment processing wrong at launch is expensive and slow to fix. This playbook walks first-time operators through the exact order of operations — from merchant account applications to chargeback management — so you go live with a stack that actually converts.

Get our 2026 cost & licensing breakdown by email.