iGaming Payment Processing in 2026: The Operator's Step-by-Step Launch Playbook

What exactly is iGaming payment processing and why is it different from normal e-commerce?

iGaming payment processing covers every transaction flow inside an online casino or sportsbook — deposits, withdrawals, refunds, and chargebacks. It differs from standard e-commerce because gambling is classified as high-risk by card networks, triggering stricter underwriting, mandatory rolling reserves, lower chargeback tolerance, and a much smaller pool of willing acquirers.

The root of the complexity is MCC 7995 — the Merchant Category Code assigned to gambling transactions by Visa and Mastercard. The moment that code appears on your merchant account application, most mainstream acquiring banks decline outright. The ones that do process gambling charge a premium: expect discount rates of 3–7% on card transactions versus 1.5–2.5% for a typical e-commerce merchant. That spread compounds fast when you're processing millions monthly.

Beyond pricing, card-network rules for MCC 7995 include hard caps on chargeback ratios, mandatory transaction monitoring, and in some jurisdictions, outright blocking of gambling transactions at the issuing bank level. In the US, the Unlawful Internet Gambling Enforcement Act (UIGEA) adds another layer — your US-facing payment flows must comply with UIGEA's transaction blocking requirements, which means most US-issued cards simply won't process at offshore sites regardless of your PSP setup.

The practical consequence for a first-time operator: you cannot treat payments as an afterthought you bolt on after platform selection. Your payment stack — acquirer relationships, PSP integrations, crypto rails, and withdrawal methods — needs to be scoped and applied for in parallel with your licensing and platform work, not after. Operators who sequence this wrong routinely sit on a finished platform with no live payment method for 60–90 days post-launch.

What is a rolling reserve and how much should you budget for it?

A rolling reserve is a percentage of gross processing volume that your acquirer withholds as a security deposit against chargebacks and fraud. For iGaming merchants, expect 5–10% held for 90–180 days. On $500K monthly volume that's $25–50K locked up per month — a real cash-flow hit that first-time operators consistently underestimate.

The mechanics work like this: if your acquirer holds 7% for 180 days, you're effectively pre-funding six months of reserves before you see the full benefit of your processing volume. In month one you receive 93 cents on every dollar processed; the withheld 7% releases six months later. Scaling aggressively in months two through six means more cash tied up, not less. Model this in your treasury plan before you sign the merchant agreement.

Rolling reserve rates are negotiable, but leverage matters. A brand-new operator with no processing history will sit at the high end — 8–10% for 180 days is common. An operator who can show 12 months of clean processing history with a chargeback ratio under 0.5% can sometimes negotiate down to 5% for 90 days. Some PSPs structured specifically for gambling (Payvision, Safecharge/Nuvei, Paysafe) have more flexible reserve structures than general acquirers because gambling is their core book, not an edge case.

One underused strategy: offset rolling reserve pressure by launching with crypto payments first. CoinsPaid, B2BinPay, and TripleA don't hold reserves — you receive settlement in near-real-time, often within hours. For an offshore operator on a Curaçao or Anjouan license, routing 30–40% of deposit volume through crypto from day one meaningfully reduces the cash tied up in card reserves. It's not a permanent fix, but it buys you breathing room while your card processing history matures.

| Operator Profile | Reserve Rate | Hold Period | Notes |

|---|---|---|---|

| New operator, no history | 8–10% | 180 days | Expect this as the opening offer from most acquirers |

| 12+ months clean history, <0.5% CB | 5–7% | 90–180 days | Negotiable; bring your processing statements |

| Established operator, MGA or UKGC license | 3–5% | 90 days | Regulated license materially improves terms |

| Crypto-only gateway (no card rails) | 0% | N/A | No reserve, but limited reach for non-crypto players |

How do you actually get an online gambling merchant account — what's the step-by-step process?

Securing an online gambling merchant account takes 6–12 weeks from application to first live transaction. The process runs: assemble your documentation package, apply to 2–3 specialist acquirers simultaneously, pass underwriting, negotiate terms, integrate the gateway, and complete test transactions. Apply before your platform is live — never after.

The documentation package is where most first-timers lose time. Acquirers underwriting MCC 7995 merchants want: your gambling license (or proof of application), certificate of incorporation, beneficial ownership structure with KYB documentation for all shareholders above 10–25% depending on the acquirer, a business plan with projected processing volumes, a sample of your terms and conditions, your AML/KYC policy, and — critically — your responsible gambling policy. Missing any of these triggers a request for information (RFI) that adds two to three weeks to the timeline.

Apply to multiple acquirers simultaneously, not sequentially. The iGaming-specialist acquirers worth approaching include Nuvei (formerly Safecharge), Paysafe, Worldpay's gambling vertical, Payvision, and CEPSA. For European-facing operations, acquirers in Malta and Cyprus tend to have more streamlined gambling underwriting than those in the UK or Germany. Be transparent about your license jurisdiction — misrepresenting a Curaçao license as equivalent to an MGA license during underwriting is a fast path to account termination.

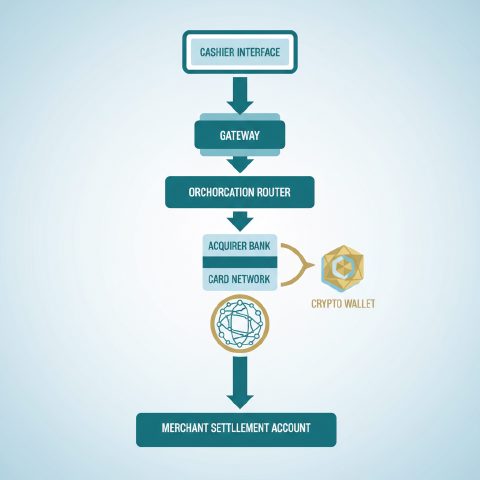

Once approved, integration is the next bottleneck. Most specialist PSPs offer a hosted payment page (HPP) or a REST API. The HPP route gets you live faster — sometimes in a week — but gives you less control over the checkout UX. The API route takes 3–6 weeks of developer time but lets you keep players on your domain through the entire deposit flow, which measurably improves conversion. If you're on a white-label platform like SoftSwiss BGCS or EveryMatrix, many acquirers are already pre-integrated — you're flipping a switch in the back office, not writing code.

Which iGaming PSPs and payment gateways are actually worth using in 2026?

The iGaming PSP market has consolidated around a handful of specialists: Nuvei, Paysafe, and PaymentIQ (Devcode) dominate platform-integrated stacks. For offshore and crypto-forward operations, CoinsPaid, Praxis Cashier, and Payneteasy fill the gap. The right choice depends on your license jurisdiction, target markets, and whether you need a full cashier or just an acquiring layer.

Nuvei is the most operator-friendly full-stack option for regulated markets — they hold acquiring relationships across 200+ markets, support 600+ payment methods, and their gambling vertical underwriting is mature. The trade-off is pricing: Nuvei is not cheap, and their contract minimums mean they're less accessible for operators processing under $1M monthly. Paysafe (which includes Skrill and NETELLER) is strong for European player bases where e-wallets dominate deposit behavior, but their merchant onboarding has historically been slow.

PaymentIQ by Devcode deserves special mention because it's a payment orchestration layer rather than a PSP — it sits between your platform and multiple acquirers, routing transactions based on rules you define. If your primary acquirer declines a card, PaymentIQ can automatically retry through a secondary acquirer. That redundancy is worth the additional integration complexity. Most serious operators running EveryMatrix or BetConstruct are already on PaymentIQ.

For crypto, CoinsPaid is the market leader in iGaming specifically — they process for hundreds of operators and support 30+ cryptocurrencies with same-day settlement. B2BinPay and TripleA are solid alternatives with slightly different coin coverage. The honest assessment: crypto gateways are the easiest payment method to get live for an offshore operator, and they're increasingly a primary payment method rather than an afterthought, particularly in markets where card acceptance rates are low.

| Provider | Type | Best For | Approximate Card Rate | Crypto Support | Onboarding Time |

|---|---|---|---|---|---|

| Nuvei (Safecharge) | Full-stack PSP + acquirer | Regulated EU/global operators | 3–5% | Yes (via partners) | 4–8 weeks |

| Paysafe / Skrill | PSP + e-wallet | European player bases | 3–6% | Limited | 6–10 weeks |

| PaymentIQ (Devcode) | Payment orchestrator | Multi-acquirer redundancy | Pass-through + fee | Via integrations | 2–4 weeks (if acquirers ready) |

| CoinsPaid | Crypto gateway | Offshore / crypto-forward ops | N/A | 30+ coins | 1–2 weeks |

| Praxis Cashier | Cashier + routing layer | Offshore operators needing breadth | Pass-through + fee | Yes | 2–3 weeks |

| Payneteasy | PSP + acquirer | LATAM / emerging markets | 4–7% | Partial | 4–6 weeks |

How do you manage chargebacks in an online casino before they kill your merchant account?

Online casino chargeback management starts before the first transaction is processed — not after you receive your first dispute. Build fraud screening, velocity rules, and a dispute response workflow into your launch checklist. Visa's threshold is 1% chargeback ratio; Mastercard's is 1.5%. Breach either and your acquirer can terminate with 30 days' notice or less.

The most common chargeback trigger in iGaming is 'friendly fraud' — a player loses, panics, and disputes the transaction with their bank claiming they didn't authorize it. Unlike physical goods merchants, you can't show a delivery receipt. What you can show is session logs, IP data, device fingerprints, and the player's acceptance of terms at registration. Build your KYC and terms-acceptance flow to generate this evidence automatically at every deposit, not just at registration. Platforms like SoftSwiss and Softgamings typically have this baked in; if you're on a custom build, it's your responsibility.

Fraud screening tools — Kount, Sift, or the built-in rules engines in PaymentIQ — should be configured before go-live, not after you see your first fraud spike. Set velocity limits (e.g., maximum three deposit attempts per hour per player), block high-risk BINs for your jurisdiction, and flag deposits from cards registered in a different country than the player's IP. These aren't perfect, but they cut friendly fraud significantly.

When a chargeback does land, respond to every single one — even the ones you'll lose. Your acquirer tracks your response rate as a sign of operational maturity. A well-documented response with session logs, KYC documents, and the player's IP/device data wins a meaningful percentage of disputes. Services like Chargebacks911 specialize in iGaming dispute representment and are worth the fee if your volume justifies it. The goal is keeping your ratio below 0.5% — that's the level where acquirers stop watching you nervously and start talking about better rates.

What's the difference between a white-label payment setup and building your own acquiring stack?

White-label platforms (SoftSwiss, EveryMatrix, Softgamings) bundle pre-negotiated payment integrations — you inherit their PSP relationships and go live faster, but you pay a revenue share and have less negotiating leverage. Building your own acquiring stack gives you full control and better economics at scale, but adds 3–6 months to your setup timeline and requires direct PSP contracts.

On a white-label setup, the platform operator is typically the merchant of record — your players see the platform's payment descriptors, and the platform handles the acquirer relationship. This is genuinely faster: SoftSwiss BGCS, for example, has Nuvei, CoinsPaid, and a dozen other methods pre-integrated. You configure which ones appear in your cashier, set deposit limits, and you're done. The cost is a revenue share — typically 10–15% of GGR — that covers the platform, the games, and the payment infrastructure as a bundle. You never see the raw PSP contracts or negotiate rates directly.

Turnkey builds (where you own the platform but use a managed service) sit in the middle. Providers like Softgamings or GammaStack will handle the technical integration but you can negotiate your own PSP contracts if you have the processing history to do so. This gives you more control over payment economics without the full overhead of a custom build.

Custom builds make payment economics sense only above roughly $5M monthly GGR, in my experience. Below that threshold, the engineering cost of maintaining direct PSP integrations, handling API updates, and managing PCI-DSS compliance eats the margin you saved on revenue share. The operators who go custom too early consistently underestimate PCI scope — if you're storing, processing, or transmitting cardholder data directly, you're looking at a SAQ-D or full QSA audit, which runs $15–50K annually plus remediation costs.

How does iGaming payment processing differ by license jurisdiction — Curaçao vs MGA vs US states?

Your license jurisdiction directly determines which PSPs will work with you, what reserve rates you'll face, and which card networks will approve your transactions. An MGA license opens doors that a Curaçao sublicense closes. US state licenses (New Jersey, Pennsylvania, Michigan) require state-approved payment processors and exclude most offshore PSPs entirely.

Curaçao (now operating under the new Gaming Control Board framework since 2023) remains the fastest and cheapest license to obtain — roughly $25–35K all-in, 2–4 months to issue. The trade-off is payment friction: many tier-1 acquirers won't touch Curaçao-licensed operators, Visa and Mastercard block a higher percentage of transactions from Curaçao-licensed sites at the issuing bank level, and you'll consistently sit at the high end of reserve rates. Crypto becomes proportionally more important as a payment channel for Curaçao operators specifically because it bypasses these restrictions.

An MGA (Malta Gaming Authority) license costs more — €25K application fee plus compliance infrastructure — and takes 4–6 months, but it materially changes your PSP options. Acquirers in Malta, Cyprus, and increasingly Lithuania treat MGA licensees as standard commercial risk rather than high-risk, which translates to lower rates and more flexible reserve terms. Paysafe, Nuvei, and Worldpay's gambling vertical all have preferred relationships with MGA operators. For EU-facing operations doing serious volume, the MGA license pays for itself in better payment economics within 12–18 months.

US state-regulated markets are a different universe. New Jersey's Division of Gaming Enforcement (DGE), Pennsylvania Gaming Control Board (PGCB), and Michigan Gaming Control Board each maintain approved vendor lists — your PSP must be on the list for your state, full stop. PayNearMe, Everi, and Sightline Payments are examples of processors active in US iGaming. Offshore PSPs don't apply. The upside: player trust and card acceptance rates are dramatically higher in regulated US markets because issuing banks don't block transactions from licensed operators. The downside: every payment vendor goes through its own state approval process, which adds months.

What does a properly structured iGaming payment stack look like at launch?

A launch-ready iGaming payment stack has three layers: a primary card acquirer, at least one alternative payment method (e-wallet or local payment), and a crypto gateway. Redundancy is not optional — if your primary acquirer goes down or terminates you, you need a live fallback within hours, not weeks.

Layer one is your primary card acquirer — this is where the bulk of your deposit volume will flow. For an offshore operator, this might be Nuvei or a regional acquirer in Cyprus or Malta. For a US-regulated operator, it's a state-approved processor like PayNearMe. Configure your cashier to show Visa and Mastercard deposit options here. This integration takes the longest to complete, so start it first.

Layer two is alternative payment methods (APMs). The right APMs depend entirely on your target market. For European players: Skrill, NETELLER, Trustly (for instant bank transfers), and MuchBetter. For LATAM: PIX in Brazil, OXXO in Mexico, PSE in Colombia. For Asian-facing operations: local bank transfer rails. Skipping APMs because 'everyone uses cards' is a conversion mistake — in mature European markets, 30–50% of deposits come through e-wallets. Praxis Cashier aggregates hundreds of APMs behind a single integration, which is worth considering if you're targeting multiple regions at launch.

Layer three is crypto. CoinsPaid or B2BinPay should be live on day one for any offshore operator. Configure at minimum Bitcoin, Ethereum, and USDT (TRC-20 and ERC-20) — those three cover the overwhelming majority of crypto deposit intent. Set auto-conversion to fiat if your operational currency is EUR or USD to eliminate volatility exposure. The integration is genuinely fast — CoinsPaid's API is well-documented and most platform providers have a native plugin. Realistically, you can have crypto live within two weeks of starting the integration.

One thing operators get wrong: they treat withdrawals as an afterthought. Players care enormously about withdrawal speed and method availability — it drives reviews, chargebacks, and retention more than almost any other operational factor. Map your withdrawal flows explicitly: which methods support payouts, what are the settlement times, and what's your manual review threshold? Automated payouts below a defined threshold (say, $500) with manual review above it is a common and sensible structure. Build this into your back-office workflow before launch, not after your first withdrawal complaint.

How do crypto casino payments actually work operationally, and what are the real risks?

Crypto casino payments route through a dedicated crypto payment gateway that generates unique deposit addresses per player, monitors the blockchain for incoming transactions, and credits the player's casino wallet — typically within 1–3 confirmations. The operational risks are volatility exposure, wallet security, and regulatory treatment of crypto gambling in your target jurisdiction.

The deposit flow is straightforward: player selects crypto, gateway generates a unique address, player sends funds, gateway monitors the blockchain and triggers a webhook to your platform on confirmation, player's balance updates. CoinsPaid and B2BinPay both handle this reliably. The key configuration decision is auto-conversion: do you hold crypto on your balance sheet or convert immediately to fiat? Most operators auto-convert to eliminate price risk. The conversion spread is typically 0.5–1.5% depending on the asset and volume — factor that into your effective payment cost.

Wallet security is the risk most operators underestimate. Your hot wallet (used for automated payouts) should hold only what's needed for 24–48 hours of withdrawal volume. The rest goes to cold storage. If you're using a managed gateway like CoinsPaid, they handle custody — but read the custody terms carefully, because you're trusting a third party with player funds. Some jurisdictions (notably MGA) have specific requirements around segregation of player funds that apply to crypto balances just as they do to fiat.

The regulatory picture for crypto gambling is genuinely uncertain in several markets. The UK Gambling Commission has signaled increasing scrutiny of crypto deposits. The Netherlands (KSA) requires licensed operators to verify the source of crypto funds above certain thresholds. In the US, crypto gambling sits in a gray zone in most states — even where online gambling is legal, the use of crypto as a deposit method may require additional compliance steps. Know your jurisdiction's position before you market crypto payments as a feature.

What are the real costs of iGaming payment processing that vendors don't put in the brochure?

The visible cost is the processing rate (3–7% for cards). The hidden costs — rolling reserves, chargeback fees, currency conversion spreads, PCI compliance, and failed transaction fees — often add another 1–3% on top. First-time operators routinely underestimate total payment costs by 30–50% in their financial models.

Chargeback fees are a particularly nasty surprise. Most acquirers charge $15–50 per chargeback regardless of outcome — win or lose the dispute, you pay the fee. At 0.8% chargeback rate on 10,000 transactions, that's 80 chargebacks per month at $25 each = $2,000/month in fees before you've even counted the lost revenue. Dispute management isn't just about protecting your account; it's a direct P&L line.

Currency conversion is another invisible cost. If your players deposit in GBP and your settlement currency is EUR, every transaction crosses a currency conversion — typically at a spread of 1–2% above mid-market. At scale, this is significant. Negotiate settlement in your primary player currency where possible, or use a multi-currency account structure to batch conversions rather than converting transaction-by-transaction.

PCI-DSS compliance cost depends entirely on your integration model. If you're using a hosted payment page (HPP) from your PSP, you're likely SAQ-A eligible — a self-assessment questionnaire that costs almost nothing. If you're passing card data through your own servers, even briefly, you're in SAQ-D territory, which means quarterly vulnerability scans, annual penetration testing, and potentially a QSA audit. That's $15–50K annually for a small operator. White-label platforms handle PCI scope for you — another underappreciated advantage of that model for operators who aren't ready to manage compliance infrastructure.

What's the realistic timeline to get iGaming payment processing live from scratch?

From zero to first live card transaction takes 8–14 weeks for most offshore operators — longer if you're applying for a regulated license simultaneously. Crypto can be live in 2–3 weeks. US state-regulated payment processing takes 4–6 months minimum because every vendor requires state approval. Plan your launch date around your payment timeline, not your platform build.

Week 1–2: Assemble your documentation package (license, corporate docs, KYB, AML policy, responsible gambling policy, projected volumes). This takes longer than founders expect — tracking down notarized corporate documents from offshore jurisdictions can burn two weeks alone. Start this in parallel with your platform selection, not after.

Week 2–4: Submit applications to 2–3 PSPs simultaneously. Don't wait for one to respond before applying to the next. Use this period to integrate your crypto gateway — CoinsPaid or B2BinPay can be live before your card acquirer even responds to your application. Set up your APM integrations (Skrill, Trustly, etc.) during this window too, as they often have faster onboarding than card acquirers.

Week 4–10: PSP underwriting. This is the waiting period. Respond to RFIs within 24 hours — slow responses add weeks. Use this time to configure your cashier, set deposit/withdrawal limits, build your chargeback response templates, and complete PCI compliance scoping. Week 10–14: Contract negotiation, technical integration, test transactions, and go-live. Don't skip thorough testing — payment integration bugs that surface after launch create player complaints and potential license violations if funds are mishandled.

The operators who hit the short end of this timeline (8 weeks) are the ones who started their PSP applications before their platform was even fully selected. The ones who hit 16+ weeks are the ones who treated payments as step five in a five-step process. Treat it as step one through five — it runs in parallel with everything else, not after it.

Comments

No comments yet — be the first.